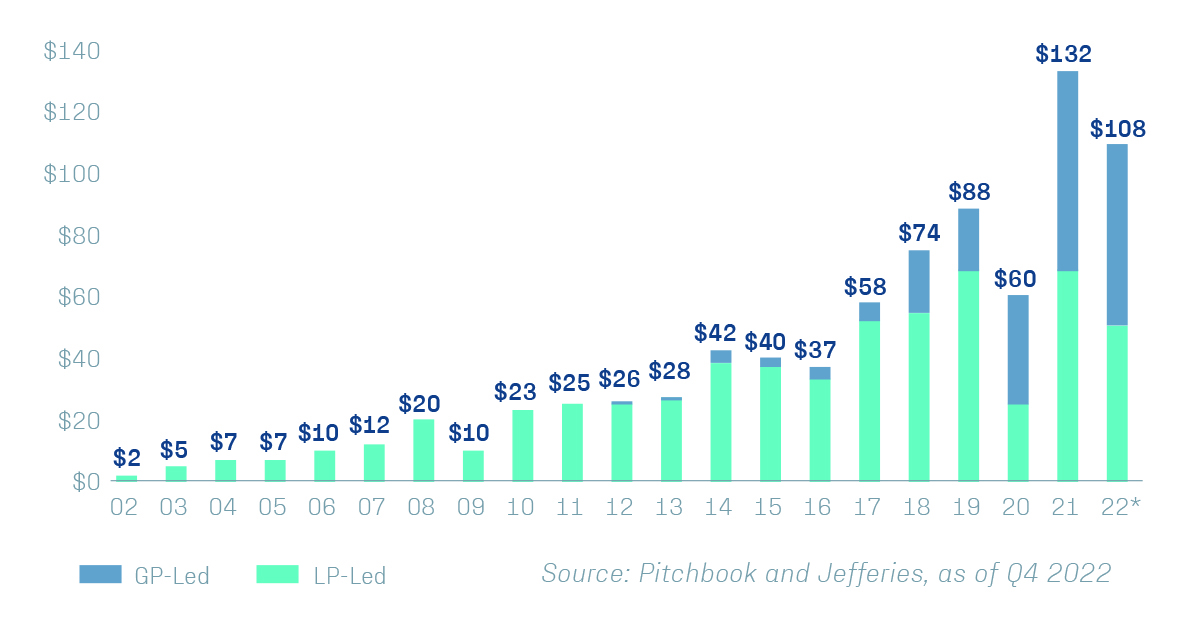

Background on the Secondaries Market

It’s well known that private capital investment opportunities are long-term investments that are highly illiquid. In other words, it can take multiple years to receive material liquidity from private capital funds, and it may take over 10 years for a fund to fully liquidate. For investors that demand liquidity, it’s challenging to find a qualified buyer and determine a fair price at which the investment can be purchased. In most instances, the manager of the fund can restrict transfers to only buyers it approves. Due to investors wanting to gain early liquidity from private capital investments, the secondaries market began to develop, starting with traditional LP transactions. The most transacted strategy is buyout, but there are secondary markets for venture, growth, credit, real estate, and infrastructure as well.

Benefits of Secondaries Funds

We believe that there are many benefits to secondaries funds that make them attractive investment opportunities, including:

DIVERSIFICATION ACROSS INVESTMENT STRATEGIES, GEOGRAPHIES, MANAGERS, AND VINTAGE YEARS. Because secondary funds have the ability to invest in mature and diverse private funds, they provide exposure to a broad range of assets. Diversified secondary funds can hold positions in over 1,000 global private companies managed by hundreds of managers.

REDUCED BLIND POOL RISK. Since secondary funds invest in funds that have already invested in portfolio companies, they do not carry the same blind pool risk as primary investment strategies

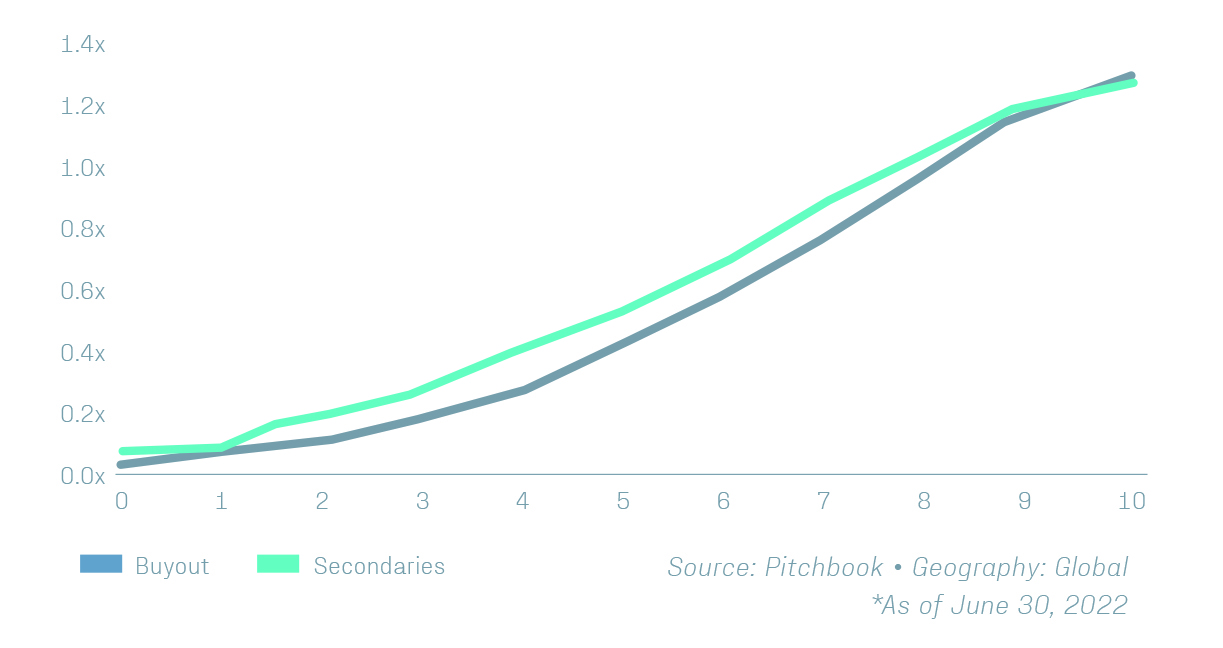

J-CURVE MITIGATION. It is common for funds to trade on the secondary market at a discount to a reference net asset value. For example, if a fund with an NAV of $100 can be purchased at $85, the return for the buyer can be 17.6% at the next valuation date if the underlying NAV is unchanged at $100. Discounts vary with economic and market conditions, as well as relative supply and demand of capital. Compared to the delayed cash-flows of primary investment strategies, secondaries funds provide investors with exposure to cash flowing assets more quickly, since they are typically investing in mature funds. Data from Pitchbook shows that material cash flows occur sooner with secondaries compared to buyout funds. A full return of capital (a distribution-to-paid-in, “DPI” multiple of 1.0) can occur 1-2 years sooner for secondaries funds compared to buyout funds.

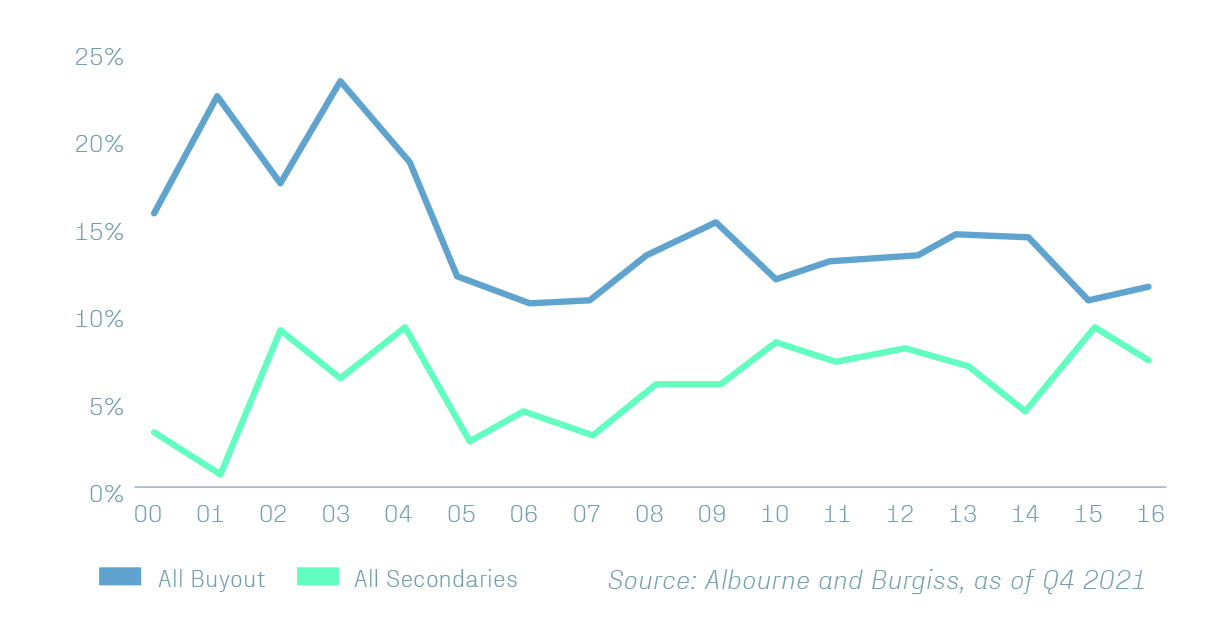

PERFORMANCE CONSISTENCY ACROSS DIFFERENT MANAGERS. The difference in net IRRs between the best performing and worst performing secondary managers is much tighter compared to other private equity strategies. This limits potential disappointment for investors in secondary funds. However, it should be noted that secondary funds typically have a lower ceiling on potential returns as well as a higher floor compared to less diversified strategies

Traditional LP Transactions

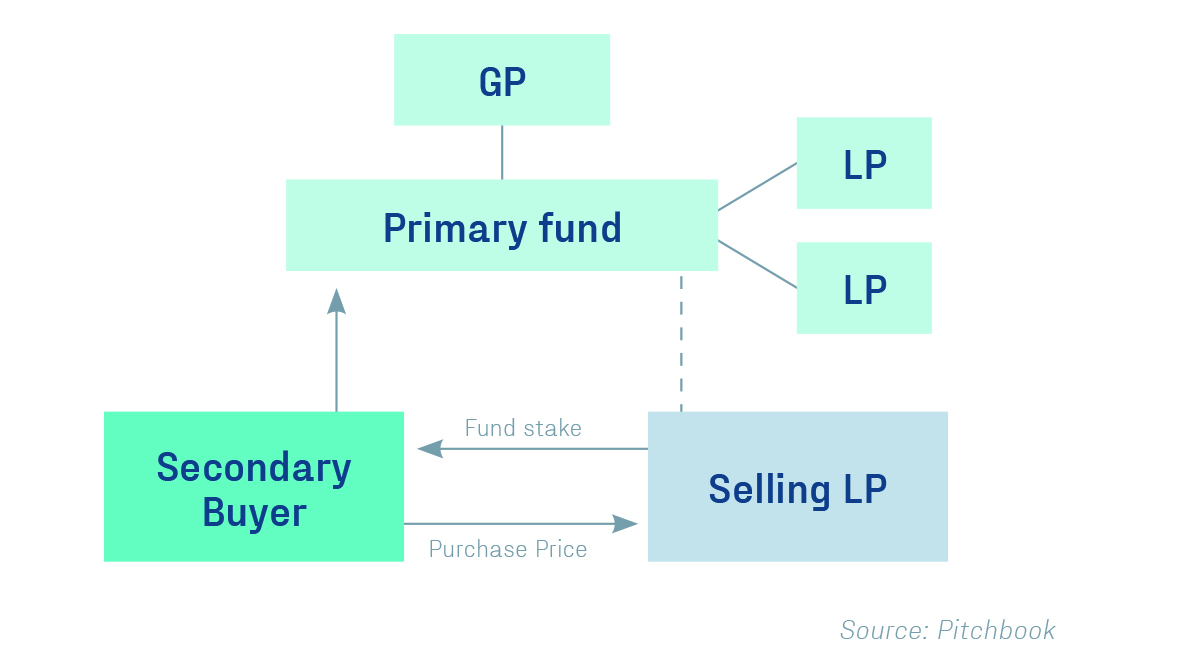

Traditional LP transactions are the most common type of secondary transaction and are also the simplest. A traditional LP transaction involves an LP in a private fund selling their investment to a different LP or a secondary fund, who would then gain control of the former LP’s investment and capital call obligations. This exchange of investment from the former LP to the new LP would have to be approved by the GP of the private fund. Since traditional secondaries transactions involve a simple transfer of ownership in a private fund investment, these deals are more effortlessly executed by secondary fund managers compared to complex transactions. Typically, LP transactions are intermediated through a broker, creating a degree of efficiency to the market.

Complex GP-Led Transactions

GP-led transactions provide additional liquidity options for LPs in private funds utilizing different methods than traditional LP transactions. These transactions are more sophisticated deal types that require differentiated knowledge and relationships to execute. GPs initiate these transactions and can be selective with potential counterparties, given the chance for reputational risk. Therefore, the complex secondaries transaction space has lower competition and a greater possibility of higher returns.

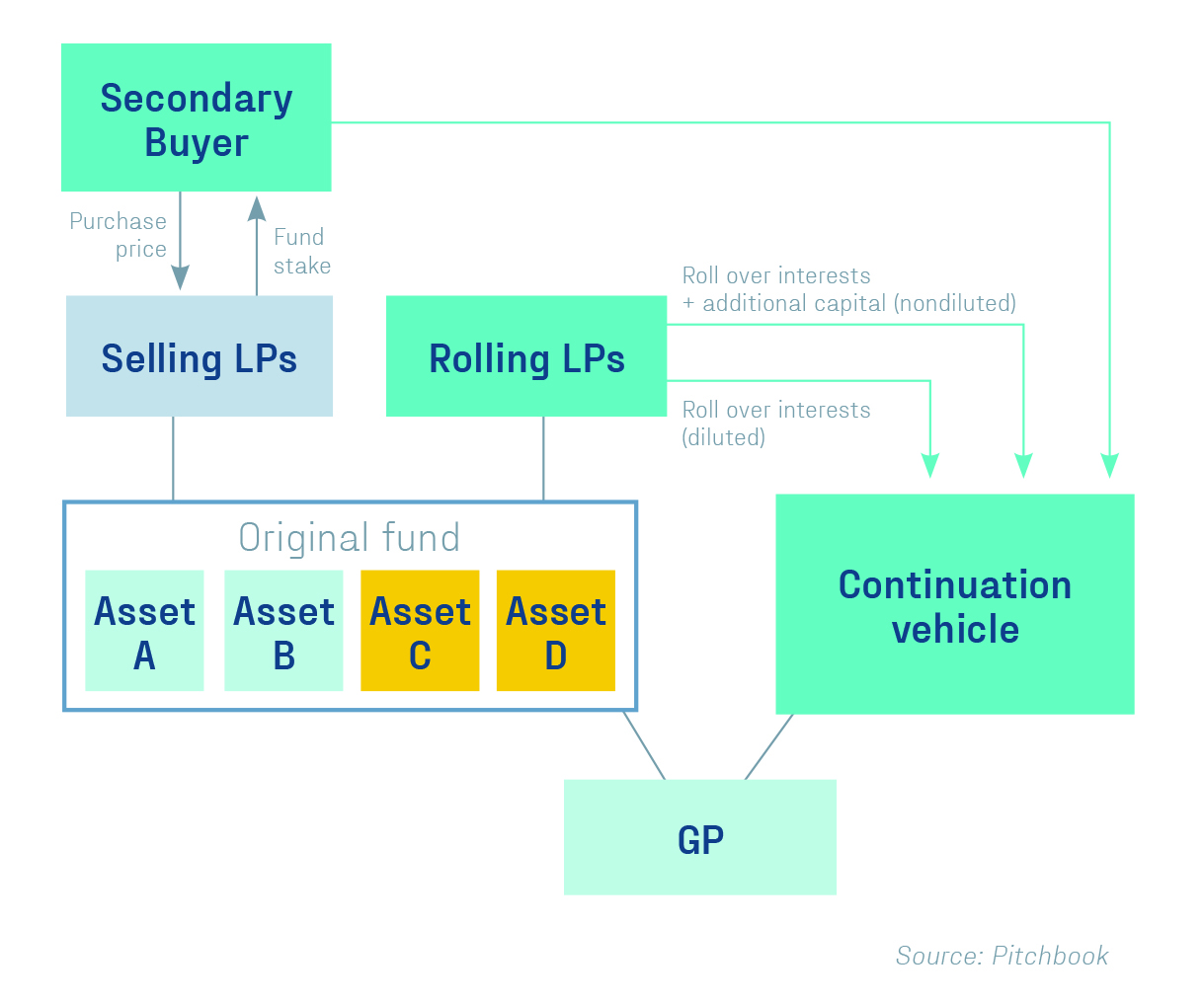

Examples of complex secondaries transactions include moving assets into a continuation fund, investment team spin-outs, direct secondary purchases from a GP, and preferred equity. As the secondaries market has continued to develop, and the return potential of complex secondaries transactions has become evident, these types of transactions are becoming more common. A popular GP-led transaction is a continuation fund that provides liquidity options to existing LPs and more time and/or capital for the GP to hold and create value for select portfolio positions. These transactions typically occur as the underlying fund is approaching its term limit. The GP works with a partner, typically a dedicated secondary manager, to provide capital to purchase the positions from those LPs seeking liquidity. The selected assets are placed in a continuation fund with new parameters including term, fees, and expenses. The assets continue to be managed by the GP, and the investor base is comprised of the GP, LPs that declined the option for liquidity, and the secondary manager that partnered with the GP. These deals typically provide exposure to a single or several assets. An example is below.

Conclusion

With the sharp growth in private capital fundraising since the Great Financial Crisis, secondary markets have grown and evolved to meet the increasing demand for liquidity from investors. In our view, secondaries can serve as a core allocation in private portfolios. Additionally, for investors earlier in their private investing lifecycle, secondaries can materially hasten diversification across strategy, GP, vintage year, and geography. Other desirable features include J-curve mitigation, quicker cash flows, and lower dispersion across funds.

To learn more about how GLASfunds makes alternative investing streamlined with our platform that brings together access, technology, sourcing, and reporting, visit: https://glasfunds.com

DISCLAIMER

This report and the information contained herein is not intended to be, nor should it be construed as, an invitation, inducement, offer or solicitation to engage in any investment activity. This information is for discussion purposes only. Nothing contained in this report constitutes tax nor legal advice. Alternative Investing is complex and speculative; and thus, not suitable for all investors. Such investment vehicles contain a high degree of risk and therefore no assurance may be made that any alternative investment objectives will be attained nor that investors will receive return of capital.

This report is an opinion only; it is not to be relied upon as the basis for an investment. Any data and firm information shown are for illustrative purposes. The information in this report has been provided to GLASfunds, including its employees, by sources determined to be reliable in providing such information. Therefore, GLASfunds has not, and is unable to, independently review, prepare, or verify information contained herein; further, GLASfunds makes no representation or warranty regarding the accuracy of the information provided to GLASfunds.Past performance is not indicative of future returns.

GLASfunds, LLC is a registered investment adviser under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training